Blog

Globally, sustainable investing assets in the US, EU, Canada, Australia and New Zealand combined amounted to $30.7 trillion in early 2018, a 34% increase in two years. In the US alone, 26% of the $46 trillion professionally managed assets, totaling to $12 trillion, are categorized as “sustainable investing” in 2018, a 38% increase compared to 2016.

So, what exactly is “Sustainable Investing”?

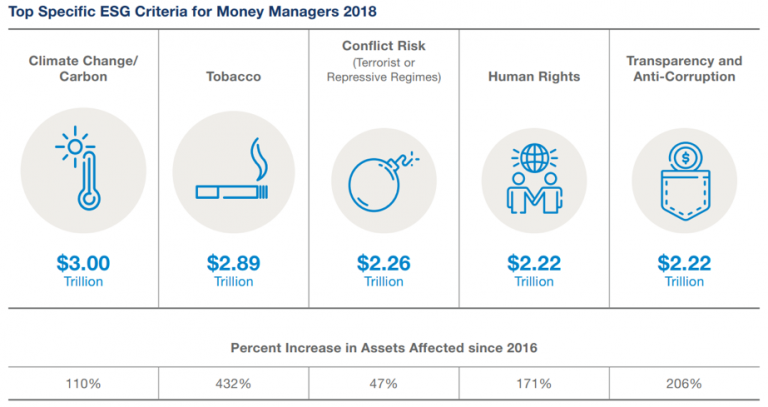

Source: Forum for Sustainable and Responsible Investment (US SIF), 2018

1. What is sustainable investing?

“Sustainable investing” is also called “ESG investing” or “(socially) responsible investing”.

Although there is no official definition or taxonomy, it is commonly accepted that the core of this type of investment is to incorporate measurable criteria in the categories of environment, social and governance (ESG) element in decision-making during the investment cycle, from investment selection, execution, supervision, reporting, to closure.

The Harvard Business Review recently summarizes the seven most common sustainable investing strategies, which can be used alone or in any combination. They are:

- Negative/exclusionary screening: excluding specific industries or countries from any investment consideration. Example: IFC Exclusion List.

- Norms-based screening: excluding companies that are not in compliance with specific norms from any investment consideration. Example: investing only companies that have adopted the UN Global Compact.

- Positive/best-in-class screening: investments only made to companies/projects with strong ESG performance. Example: investing only stocks/companies in the Dow Jones Sustainability Indices.

- Sustainability-themed investing: investments only made to companies/projects with a sustainability focus exclusively. Example: investing only renewable energy or only climate adaption projects/companies.

- ESG integration: embedding ESG considerations in investment decision-making, and monitor the ESG performance throughout the investment cycle. In other words, the ESG factors are part of the fundamental analysis from screening to closure, and everything in between. Example: The Equator Principles, IFC Performance Standards, and World Bank Environmental and Social Framework.

- Active ownership: asset owners working directly with portfolio companies to ensure their investment portfolio.

- Impact investing: investments with the intent to contribute to measurable positive social or environmental impact, alongside a financial return. See my blog on IFC’s Impact Investing Principles.

Investors can decide which strategies to adopt based on their risk appetite, ESG strategy and the desire to diversify their portfolio.

- What is sustainable investing not?

Sustainable investing is not forgoing financial returns for environmental or social impacts. In 2018, 93% of impact investors reported performance exceeded or in line with their financial expectations, according to the Global Impact Investing Network (GIIN) latest investor survey.

Sustainable investing is not sacrificing one ESG factor to peruse the other. For example, if a fund is investing in clean water, it still needs to pay attention to its labor practice. ESG should be integrated with balance, while some projects might emphasize one factor over another, all three aspects – environmental, social, and corporate governance – should be considered adequately.

- Who is sustainable investing for?

Sustainable investing is for investors. Bank of America, the largest US bank, suggested that sustainable investing stocks are more likely to have significantly higher three-year returns compared to their peers. Barclays, the world’s most powerful transnational corporation, concluded that “sustainable investing has been beneficial to bond returns”. When the investing targets in the developing countries, according to BlackRock, ESG focus investment in the emerging markets has a 9.1% of annualized return, versus 7.8% for traditional financing.

Sustainable investing is for the hosting governments. One of the criticisms to international investment is that although developing countries are benefiting from economic development, they are also suffering from the devastating environmental and social damages that directly caused by the investments. Taking ESG factors in consideration in project design and implementation will increase the positive social, economic, and environmental impact and reduce the potential damage to the host countries’ environment, ecosystem, labor communities, and society.

Sustainable investing is for the earth as one unity. $23 trillion private investment is needed for climate-smart projects in emerging markets alone to combat climate change. Furthermore, private financing is crucial in pulling the 783 million people out of the US$1.90/day poverty line. Sustainable investing will enable the financial sector to contribute to these critical missions without compromising other E&S aspects at the same time.

- How to conduct sustainable investing?

Based on an investor or a fund’s mission and desire to create positive impacts, it can adopt one or a combination of the strategies listed above.

There are a few widely adapted international ESG finance principles/frameworks for investors – you might consider becoming a signatory, model your policies after them, or use them in your investment practice directly.

- UN Principles for Responsible Investment

- Equator Principle

- IFC Performance Standards and Operating Principles for Impact Investing

- European Investment Bank Environmental and Social Standards & Handbook

- UNEP FI Principles for Sustainable Insurance

- ICMA Green Bond Principle

Moreover, senior management endorsement, stakeholder support, and well-design systems are crucial in carrying out the sustainable investing commitment. It is also essential to dedicate staff and other resources to maintain, monitor and report on the ESG performance.

- What can government to do promote sustainable investing?

There are several things that governments can do to promote sustainable finance.

- Including sustainable development, NDC and/or UN SDG in national priorities: Explicitly citing languages from the UN Sustainable Development Goals (SDG), including the Nationally Determined Contribution (NDC) target, and using the actual phrase “sustainable development” in national priority-setting documents signals the government’s determination, guides the national legislation direction, and incentives the sustainable investing market to grow.

- Strengthening environmental and social (E&S) regulations & enforcement: Having stringent E&S regulations and effective law enforcement increases the risks and costs of potential E&S damages, and in turn, provides financial reasons for investors to be cautious of the E&S implication of their investment. Higher national standards also provide a level playing field for investors who comply with international standards.

- Provide financial and non-financial incentives for sustainable investing: The government can also incentivize the investors to conduct more sustainable investing by providing monetary benefits or non-financial recognitions. Common tools include, but are not limited to: (1) tax incentive for sustainable finance, especially for sustainability-themed sectors, such as renewable energy, clean water, and green building; (2) policy or procurement preference for sustainable invested projects or products, such as lower thresholds in granting permits or giving preferential treatments to bidders with better ESG records in government projects; (3) positive acknowledgement for outstanding performers in sustainable investing by awards or other forms of public recognition.

- Promoting non-financial information disclosure: Non-financial information usually refers to ESG information, such as environmental protection, treatment of employees, respect of human rights, anti-corruption, and diversity on company boards. Disclosure includes 3 categories: (1) the company’s ESG policies and procedures; (2) the company’s own ESG performance; and (3) the ESG performance of its investment portfolio. Examples include the EU’s Directive of Non-Financial Disclosure.

- Utilizing international resources: Developing countries can learn from developed countries and each other to accelerate the development of sustainable investing policies and markets by: (1) directly referring to or using the language/standards from international standards, such as the ones mentioned in the question above, in their national policies and standards; (2) inviting international agencies, such as World Bank or UNEP, to help policy design and implementation; (3) joining global voluntary knowledge sharing and peer-to-peer learning platforms such as the Sustainable Banking Network, Network of Greening the Financial System and Alliance for Financial Inclusion.